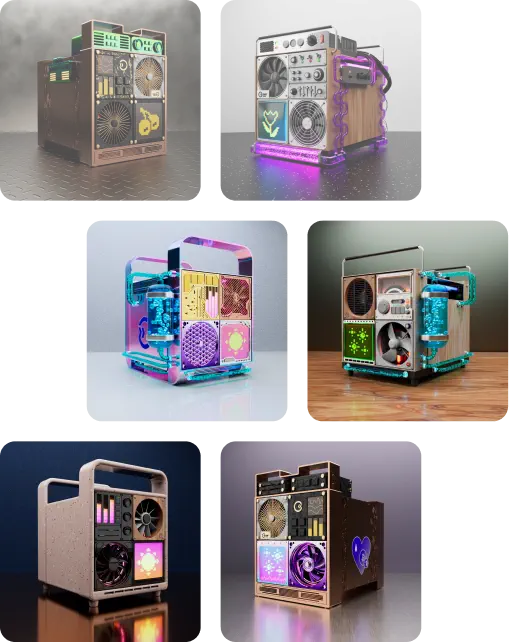

The first NFT collection of virtual miners released in collaboration between GoMining and the Trust Wallet platform. Each NFT is backed by hardware of real data centers and mines BTC every day.

GoMining Whales is a limited-edition NFT collection created in collaboration with TON. It is the first series of virtual miners on this network that mines BTC every day.